The virtualisation of the European financial system: towards a new stage of disintermediation

The IMF and the international financial institutions are preparing reforms of the international monetary system, which must also take into account this double injunction of efficiency (thus of modernity and openness to the world) and of acceptability (thus respect for sovereignty). We have already drawn our readers’ attention to Christine Lagarde’s very important speech last November concerning the creation of Central Bank Digital Currency (CBDC).[1] It is now time to return to this discourse and examine it in the light of the subject that interests us today, namely the future of European private banks.

First of all, it is important to note that the proposed revolution involving the digitisation of state currencies is a long-term one since, according to the experts, this solution should not be deployed before 2025-2030.[2] Transformations of this degree take a long time, of course. Moreover, since this speech, there has been a change in attitude concerning cryptocurrencies: Benoît Cœuré, known to have called cryptocurrencies “devils” in November 2018,[3] has now decided, along with his peers, that cryptos do not actually threaten financial stability.[4] Since then, surprise, surprise, cryptocurrencies have taken off.[5] If the big increase of the end of the year 2017 was the result of a real popular success, which we had anticipated would only last so long as the financial authorities allowed it to, this new episode is without doubt much more concerted. The innumerable private and public experiments with digital currencies are now serving as an in vivo laboratory for the reform of the world monetary system.

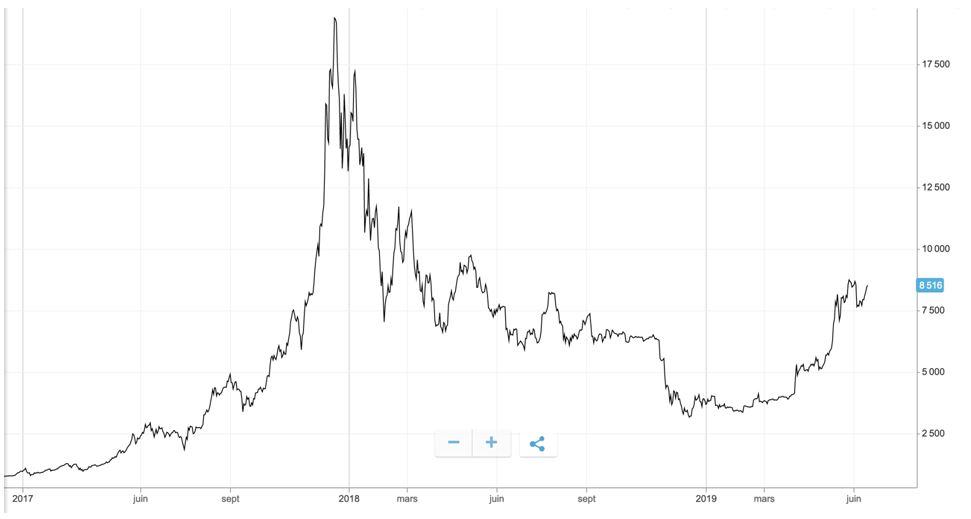

Figure – Bitcoin price in USD, 2017-2019. Source: Etoro.

Figure – Bitcoin price in USD, 2017-2019. Source: Etoro.

More than that, our team believes that they are now being used as an innovative and decentralised means (under the supervision of the financial system, but out of their legal responsibility) to create non-debt-based money supply, thus solving the problem of the 184 trillion world debt,[6] as we will show.

This brings us back to our famous private banks, rightly accused of being mainly responsible, through their loan decisions, of a creation of a cashless money supply whose key flaw is that it goes hand in hand with an increase in the indebtedness of the countries they belong to.[7]

Login