International Finance: Decentralised QE (throwback to our anticipation)

Have you noticed that all the efforts to regulate debt, derivatives, banks etc., made following the subprime crisis and meeting with varying degrees of success over the last ten years, are currently systematically undermined, including by the most serious players in the financial system? Here are some examples:

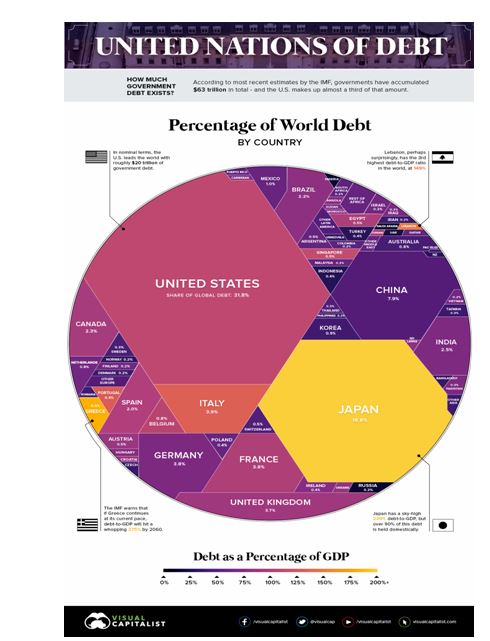

On the public debt side, the United States has just crossed the $22 trillion line, only one year after crossing the $21 trillion line,[1] clearly abandoning any attempt at reduction.

The yellow jacket crisis forced Emmanuel Macron to sign a cheque for 11 billion euros in support of purchasing power, not to mention the expenses incurred by the demonstrations and various damages, raising the French deficit from the 2.8% of GDP originally forecast for 2019 to 3.2% or 3.4% – that is 0.2 to 0.4 points above the European legal limit.[2]

Of course, there is also Italy, the third largest economy in the eurozone and one of the most indebted countries in the world (fourth position, 132% of GDP), whose ‘populist’ government, whilst having a country to run, does not intend to abide by the austerity injunctions imposed by higher authorities (Europe, Germany, IMF…), preferring to consider selling its gold reserves or to question the sacrosanct independence of its central bank.[3]

And then there is Japan with 10 trillion debt of its own, or $79,000 per capita, a country which will issue another $296 billion of government bonds at the end of its fiscal year at end of March.[4]

The United States, Europe, Japan: who can afford to give lessons to whom about sound financial management?

Figure – Public debt of countries as a percentage of global public debt. Source: Visual Capitalist.

The big question is: who buys this debt when everyone is selling it? The answer is, of course, the states themselves, through money creation. In fact, quantitative easing (QE) is in full swing more than ever, despite the tightening postures displayed by the Fed and the ECB. Has the QE simply decentralised into an economic system which simply can not stop?

Along the same lines, derivatives, the first to be blamed for the 2008 crisis, have now become virtuous products, vectors of financial stability and security by the payment guarantees they provide to economic players. So much so, that the European Commission has just announced, as part of its EMIR financial regulation programme, a simplification of the rules concerning OTC derivatives in order to reduce costs and procedures for market players. However, we know that derivatives are intended to make future payments present, thus putting an even greater burden on the future economy.

Monetary tightening by raising interest rates via central banks is no longer relevant either, since even the Fed has changed its tone on this issue. The IMF has just published a report suggesting a system of dual currencies (cash and digital) as a mechanism that will allow further progress on the issue of negative rates.[5]

In short, if the little spendthrift countries like Greece have had to bite their tongue and bear the brunt of heavy policies of austerity, as soon as Italy or France become the spendthrift countries, it is up to the small world of finance to bite their tongues.

The huge leap of faith that we are currently seeing is the obvious motivation for all the whistleblowing on the arrival of a new financial crisis.[6] But, as we have been saying before, this crisis, unlike that of 2008, has been anticipated: are these alerts really calling for greater financial rationality on the part of the major economic players (in which case there is cause for concern)? Or are they intended to encourage them to prepare for the major shock of an organised transition?

In any case, turmoil will increase right up to the tipping point. We recommend the utmost prudence in financial matters in the coming months. The more adventurous will be able to play roulette on very short-term speculative transactions, taking advantage of the high volatility that serves this kind of strategy. The more cautious will most probably stay safe with assets/securities that are as solid as possible.

Register to read the GEAB 132 in full

________________________________

[1] Source: RealClearLife, 13/02/2019

[3] Source: SeekingAlpha, 14/02/2019

[5] Source: Bloomberg, 06/02/2019

[6] IMF (source: CoinGape, 04/10/2018); JPMorgan (Bloomberg, 13/09/2018)

Login