Europe has long benefited from a powerful economic engine: the household savings.

Built up over decades, this financial cushion, estimated at 35.5 trillion euros (against 14 trillion public debt), has served both as a buffer in times of crises and a vital source of funding for the major transformations ahead – the climate transition, reindustrialisation, defence, innovation, and more.

This “pactole“[1] as the French would say, is therefore the subject of numerous attempts to mobilise it. At European level, last November, Christine Lagarde was clear about strategy aimed at bringing together capital markets, mainly to channel savings towards innovators at European level as part of her “Kantian revolution”[2] (since then, Europe has voted 800 billion for armaments…).

At national level, tax incentives (even punitive for tying up capital) and ad hoc financial products are aimed at savings out of their wallets. The aim, of course, is for savers to boost their capital and grow richer at the same rate as the continent will grow richer if this funding is properly managed. Some key questions on this topic:

- Is the EU able to produce a vision accurate enough of its future to channel these savings correctly?

- Is it also well equipped to guarantee a return on investment for savers and no-one else?

- Finally, do Europeans have enough confidence in the European institutions to play the game?

If these conditions are not met – and we have every right to doubt that they will be – the savings of European households could be part of a silent drain, siphoned off by all the European, national and stock market smoke and mirrors. If this is the case, by 2030, Europe could find itself naked, overtaken by larger and faster players, without natural resources, still dependent on others for technology, relatively uncaptive of foreign capital (especially in the context of the ongoing reconfiguration of financial flows[3]), with an unattractive consumer market because it is impoverished, and moreover stripped of its savings cushion.

If Europe loses the last of its major levers, it will have to cope with an irreversible loss strategic autonomy. This increased dependence will not just be economic, it will also be political and geopolitical. Up until now, the cushion household savings has made it possible to maintain social stability and a crisis buffer. Converting it into a lever for investment can only be done with a clear, shared and protective vision.

Savings as the ultimate lever

Faced with out-of-control budget deficits and virtually no room for manoeuvre, Europe is preparing to use private savings as the ultimate economic lever. But this plan, which might seem a salutary solution, could also set the stage for a spiral of major vulnerabilities. We even anticipate that from 2026 onwards, the drain of this lever, combined with popular reactions and economic transformations around the world, will lead to a massive flight of capital out of Europe.

This anticipation is based on trend observation. Over the last fifteen years, successive crises – the financial crisis of 2008, the sovereign debt crisis, the Covid-19 pandemic, the war in Ukraine, the inflationary surge – have undermined Europe’s public finances, raising average public debt to over 80% of GDP and the deficit to 3.6%.

Today, even the richest EU countries are affected, including Germany, now the region’s sick man[4]. The time has therefore come to look for new levers, and among the various solutions, mobilising savings – which has been on the papers for some time now – appears to be one of the main ones.

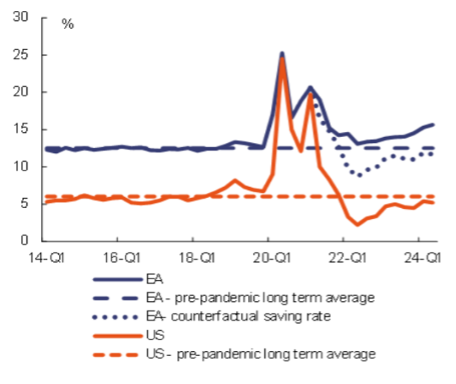

The savings accumulated by European households represent a logical target. EU countries are among the biggest savers in the world, with total savings in the region estimated at 35,500 billion euros (this figure varies depending on the analysis), or around 15% of disposable household income (compared with 4% in the United States, for example). Faced with the current challenges, the objective of the European and national authorities is twofold:

Firstly, to transform these precautionary savings into productive investment, without triggering capital flight or destabilising the banking system.

Secondly, with the parallel help of inflation, to reduce the level of public debt in the Eurozone and thus limit the interest rate differentials between European countries – the main threat to the ECB and the economic authorities. Implementation of the savings mobilisation project will therefore accelerate this year.

Under the impetus of the European Commission, Capital Markets Union, long paralysed by differences between Member States, will be adopted under the banner of “Savings and Investment Union”, as already proposed[5].

Initially, this project will be implemented in a way that can be described as ‘soft’, using various incentives: tax deductions (as is already the case in France for green investments), pension plans, performance bonuses, partial tax exemptions on capital gains, etc.

Household saving rate comparison, Eurozone / USA. Source: Eurostat for EA, Bureau of Economic Analysis for US.

At the same time, national tax policies, which are likely to be increasingly centralised in Brussels[6], will massively encourage investment in financing on a European scale: defence[7], artificial intelligence[8], or the ecological transition (along the lines of the Green Pact, now somewhat at a standstill)…[9]

But the ideal mechanism for channelling savings to the European level is, of course, the digital euro, a project which is now making good progress[10] and which looks set to be deployed closer to the end of 2027[11].

The ECB’s digital euro will play a pivotal role. Originally presented as a simple instrument for modernising payments, it will become a steering tool for the savings and investment union.

It will provide better traceability of financial flows, direct deposits towards certain types of assets, and cap the amounts saved in non-risky vehicles. In other words, all of these functions are part of the project to mobilise savings to meet Europe’s financial challenges.

2025-2027: The great divide

Down the road toward 2027 (in the best-case scenario), there are two years which, according to our forecasts, will be fraught with major difficulties for Europe:

. Coming out of the war without exploding in mid-air in the wave of enlargement that will follow.

. Succeeding in repositioning itself in the emerging multipolar world.

. Fitting properly into the next international monetary system.

. Remaining attractive in a fast-moving world focused on finance and talent.

. Freeing itself from a legal straitjacket that is slowing us down, without losing sight of our values (democracy AND law).

. Setting up a defence and peace architecture.

. Deploying proprietary technological infrastructures.

. Securing our strategic supplies.

. Reinventing an obsolete social system to maintain our last argument, namely our consumer market,…

Faced with so many challenges, there is a risk that the massive redirection of savings will simply keep the EU’s head above water without any leverage, in which case the first signs of exhaustion would soon appear.

A vicious domino effect

From 2026 onwards, the returns offered to savers could remain structurally low, once adjusted for inflation. As a result of these unattractive returns and widespread impoverishment in the Eurozone linked to rising prices, there is a risk that savings will be channelled outside the EU or into non-productive assets: offshore crypto assets, foreign equities, physical gold, non-EU property, etc.

However, the arrival of the digital euro, issued by bodies far removed from the public, will increase mistrust and rejection, particularly in a context where the United States may have strengthened the credibility of crypto currencies such as Bitcoin in place of Central Bank Digital Currencies (CBDC)[12].

To remain attractive, the ECB will have to keep interest rates high to maintain its currency, attract foreign capital and retain domestic money, which will have consequences for public and private financing, reducing the capacity to cover deficits. Increased dependence on capital from outside Europe – particularly from the United States – will expose Member States to new refinancing risks in the event of a major shock, previous financial crises have illustrated (the 2008 crisis, the Covid-19 crisis, and the collapse of Crédit Suisse following the turbulence in US regional banks).

In this context, European banks would become increasingly dependent on international financial markets. Their capacity to finance the real economy would be reduced, which would weigh on productive investment and employment. The EU could sink into a downward spiral of constrained growth, in other words a recession, where budgetary logic takes precedence over social objectives.

Towards a destabilisation of the European banking system

In absence of a banking architecture capable of absorbing a massive transformation of savings, Europe could face an internal credit crunch. Banking disintermediation, combined with regulatory fragmentation, would weaken investment flows. Undercapitalised banks would reduce their exposure, while non-European capital markets would become the natural exit route.

This transfer could be accentuated by geopolitical dynamics: by 2030, the BRICS and their partners will have set up their own sovereign investment systems (trans-regional funds, digital money platforms, etc.). If these instruments offer a combination of returns, political stability and disconnection from Western cycles, they could capture a growing share of European savings, with the paradoxical effect impoverishing Europe in the name of its own financing.

In conclusion, a political decision above all

The future of European savings lies on a crest. Either it becomes a collective engine serving a shared vision of the future, or it is captured in an unstructured way, at the risk fuelling impoverishment and mistrust. We believe that the technocratic logic currently at work alone will not win the day in the strategy to capture savings. Europe also needs political legitimacy. The stakes are immense, and they will determine Europe’s ability to define itself as a sovereign and attractive power in the world of 2030.

______________________

[1] Used to designate a source of wealth, the term “pactole” has its origins in antiquity. It refers to the river Pactolus, in Lydia (an ancient region of Asia Minor), reputed in ancient times to carry gold. According to legend, King Midas lost his famous ‘gift’ of turning he touched into gold. Source: Wikipedia

[3] See our article on the “End of the market law”.

[6] Source: European Commission, 18/12/2024

[7] Source: European Commission, 19/03/2025

[8] Source: European Commission, 11/02/2025

[9] Source: Le Monde, 28/06/2023

[11] Source: Forbes, 07/03/2025

[12] Source: The Paypers, 20/03/2025

35,500 billion euros is the total amount of European savings. It's also the level of US federal debt. In twenty years, that debt has gone from 5% to 123% of [...]

Stock markets are reeling in the wake of Donald Trump's thunderous announcements. Is the US ruled by an erratic and reckless leader? Or are we witnessing the emancipation of politics [...]

At the crossroads of a Russian past, an American present and a European future, Ukraine, which for the last 3 years has been a testing ground for the wars of [...]

The dread of the climate crisis could soon be replaced by that of a "global seismic crisis", i.e. a gradual increase in the number and severity of earthquakes. If we [...]

After almost 20 years of anticipating the collapse of the Western-centric system, the GEAB now feels it has a duty to continue to identify the crises in the making, but [...]

As in every stock market crisis, stocks will change hands. Insofar as the crisis is largely provoked, it is likely that state structures - starting with the United States - [...]