GEAB 155

The post-Covid world is multipolar, with at least three of the major poles competing for mineral resources and industrial production. Until recently, this competition was mainly reserved for the western poles – the United States and Europe. But a third continent has joined those two: Asia.

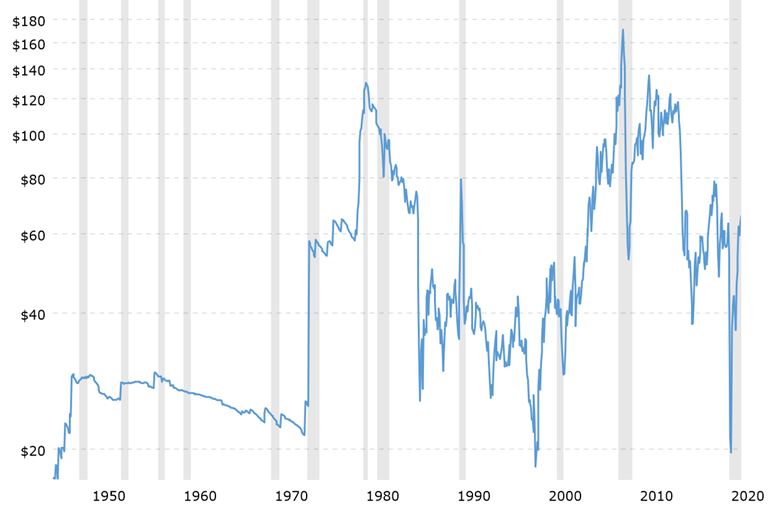

The trend is inexorable. For the past 20 years, the world’s need for raw materials has exploded at the same rate as the growth of the global economy in a limited world. Prior to each crisis, one can notice a sharp rise in the trade – and therefore the prices – of raw materials. From a systemic point of view, the 2008 crisis, to name but one, is closely linked to the quadrupling of oil prices in 6 years (2002-2008).

The graph below clearly shows that the natural trend is upwards, but reality seems to be painfully reminded each time prices recover: the financial crisis of 2008, the geopolitical (Euro-Russian) crisis of 2014, the health crisis of 2020…

Fig. 1 – Oil price curve over 70 years – Macrotrends, 2021

But ruins, wars, pandemics… nothing helps, invariably everything goes up again as soon as the danger seems to be receding.

Lost time cannot be made up for

The arrival of 4.5 billion Asians[1] in the Western economic model was anticipated, no doubt about that. Environmental agendas and the digitalisation of our societies came to reduce the material and energy burden of this economic system. But inevitably these projects to dematerialise growth could not be to everyone’s liking, and the interests they offended were powerful: the efforts to reform the model were too expensive to be accessible to all (United States), not to mention that they could be fatal for certain sectors (oil companies, etc.).

As the investments in transition were much higher than those in communication, big interests contributed to deviating the climate agenda, proposing false solutions, disturbing the rationality of a public opinion easily manipulated by the media in their hands, preventing leaders from taking the right decisions, radicalising a growing mass of afficionados advocating more and more the “economic suicide of the West” … All of the aforementioned resulted in about twenty partly wasted years of taking too few decisions, not always the right ones, and often going back on them.

As for the indispensable investments in the technologies of the future, they have given rise to what we have called a ‘futuritis’[2] (or hysterical crisis of the future) which has directed capital towards the most fantastical projects (hyperloop, space travel, colonisation of Mars, etc.) rather than towards the more austere research into new materials, innovative energy technologies (such as thorium), or classical high-speed rail networks.

2020-2040 – Energy perspectives

Our research on realistic energy futures to feed a world economy of say 5-7 billion people over the next 20 years (i.e. the growing ‘urbanised’ part of a growing world population), if we eliminate the delusional dreams of generalised degrowth to which neither the Indians, nor the Chinese or the Africans, … will of course consent, suggests in the best case the following evolution:

. a decarbonisation that prioritises a real reduction in coal, a stabilisation of oil (which is still a long way off) and a measured increase in gas (to compensate for the first two)

. a diversification of standardised energy sources thanks to the deployment of electrical cable grids, connected by artificial intelligence, regulating loads from all types of sources: hydroelectric, wind, solar, nuclear, gas power stations, etc.

. an electric-hydrogen linkage to resolve the issues of storage and off-grid power supply, while resolving the thorny problem of battery pollution.

. energy savings at all stages of the extraction-transformation-distribution-consumption-recycling/disposal cycle (and ideally a reduction in consumption in line with inflation).

It is likely that in 20 years’ time such a model will be in place. But in the meantime, the following points are still missing from the picture:

. recourse to gas: complicated because of geopolitical sensitivity (remember that among the largest gas producers are Iran, Russia and China, even if the United States is now the world’s largest producer of LNG)[3]

. nuclear power still in crisis: having lost at least 10 years of research and serious investment (small units, fusion, thorium… nothing is really ready)

. renewables: gigantic size and cost of the transition

Login

Our universe is an ever-changing web of abundant energy, it is a central aspect of life and all human activity. Yet if we see energy through the lens of our [...]

To tackle a subject as complex as energy, the LEAP teams called on the collective intelligence of the GEAB, through the GEAB Café of 20 April, and the active participation [...]

The price of the 2nd most traded commodity (oil being number one) is soaring. At a time of recovery and infrastructure plans, and illustrating the "back to basics" trend, iron [...]

One piece of business news with political significance: French and Italian media giants Vivendi (Bolloré) and Mediaset (Berlusconi) are throwing in the towel on their differences, each going their own [...]

Crypto-currencies: Maximum mistrust // Dollar : Standardisation // Technology stocks: Too virtual // Iron ore: Volatility in sight // Oil: Agility, security // If the “back to basics” trend that [...]