GEAB 181

“Be greedy when others are fearful”[1]

The great feature of 2024 is its jam-packed electoral calendar. This year, almost three billion people will be voting in 76 countries, including major ones like India, Indonesia, South Korea, Japan, Russia, South Africa, Algeria, Rwanda and, of course, the United States.

All these countries find themselves in a political stand-by phase during which few decisions will be taken, even if visions of the future will emerge – something to be followed closely. In terms of international relations and diplomacy, it will be difficult to implement strategies in such a context of political uncertainty.

Considerably complicating matters is the fact that the final election in this series, the U.S. presidential election, occurs last. As a result, any potential political changes will be enacted without a clear understanding of the political, economic, and geostrategic directions that the foremost global power might adopt by 2025. Two trends stand out:

. Strategic paralysis, on the one hand: part of the world (particularly the Western world) will go into a “wait-and-see” mode before setting off again with more elements;

. On the other hand, the United States will be less taken into account: when the other part of the world (BRICS and Global South) will take advantage of this stasis to advance its pawns, without taking into account an America and a Western world that are busy elsewhere.

From a systemic point of view, this dual trend makes it possible to anticipate:

. Major steps forward made by the BRICS, who will be seen as geopolitical players facilitating structural reconfigurations and inventing new methods of global governance;

. A widening gap emerging between leaders and citizens in Western countries, characterised by citizens’ sense of urgency regarding pressing issues, contrasting with the more cautious and wait-and-see approach adopted by leaders.

Hence, the upcoming year in the Western nations is poised to be profoundly political, marked by significant risks of public dissatisfaction. The mitigating factor lies in the potential for democratic expression through elections, albeit only conducted in specific countries and involving a diminishing portion of the population, thus paving the way for the rise of the extreme right.

In contrast, in nations closely tied to the BRICS dynamics, the focus of the year will predominantly be geopolitical. Populations in these regions will likely view promising prospects, leading them to be more lenient towards certain democratic shortcomings. Additionally, it’s worth noting that the Western-style democratic model is no longer an aspirational ideal in this “other world.”

We therefore anticipate a year of geopolitical alerts designed to shake things up, but in a controlled manner. The virulent reactions of the Western camp are bound to frighten us every time. But in the end, we expect more fear than harm in 2024.

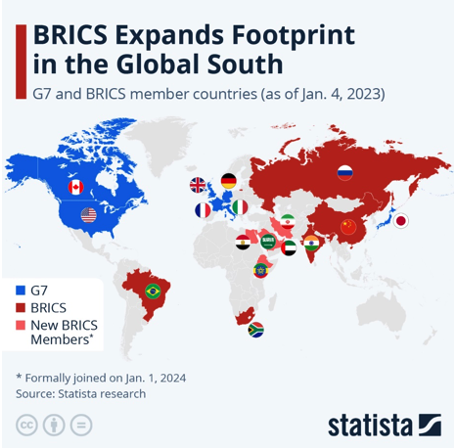

Figure 1 – Geographical comparison of G7 versus BRICS+ Source: Statista

Geopolitics: Points of stalemate and resolution

The points of uncertainty are the Ukrainian and Israeli conflicts, which could drag on for another year:

. Israel estimates the chances of resolving the conflict on its terms by 2025 (institutional elimination of Hamas – and probably Hezbollah); a Gaza Strip under Arab trusteeship.

. Russia suggests the possibility of a conflict persisting for another five years, a “threat” that may not warrant excessive concern. This is underscored by the influence exerted by China on Russia. The activation of China or another global player becomes a significant consideration, especially as the United States diverts its attention from the Ukrainian issue. Europe finds itself constrained by the fate of Ukraine, and the resolution of the conflict is anticipated as a trend leading up to the American election, potentially concluding by the end of 2024.

As for the major geopolitical flashpoints:

. Taiwan has just elected a President in the anti-Chinese vein of the outgoing presidency, who will defend the island’s political sovereignty in the face of China’s ambitions, and who must be forced to admit that his role will have to be played differently.

. This is a role offered to it by North Korean provocations, which it has an interest in containing if it wants to take advantage of a stable neighbourhood for flourishing regional trade. China, but also South Korea (helped by a legislative election that will express a desire for national unity[2], reinforced by growing concerns about inter-Korean confrontations[3]) and Japan, will see this as an opportunity to find a lasting solution to this “lock” on peace, one of the first signs of which was the resurrection of the CJK trilateral agreement (China, Japan, South Korea) to end 2023[4].

. Far from rekindling Sunni-Shiite antagonism, the Islamic State’s claim to responsibility for the attack on the Soleïmani tomb brings Iran closer to the regional anti-terrorist plan (remember our long-standing analysis: the Islamic State is the common enemy of the region instead of Israel).

As for the geopolitics of small steps:

. Ethiopia has imposed its access to the sea, and Somalia’s indignation will do nothing to change this; on the other hand, Somaliland, which until now has only been recognised by Taiwan, is gaining international recognition (especially from Africa)[5].

. Azerbaijan and Armenia are on the road to integration of the South Caucasus region – as soon as France stops supplying arms to the Armenians.

. Venezuela is trying to recover 7/10ths of Guyana; if it succeeds, Surinam could try to recover its own claim area; Guyana’s future is therefore at stake; the return of England to the defence of its former colony…

In the realm of global governance, the crucial efforts to reform international institutions such as the United Nations and WTO will continue to falter, contributing to the ongoing discrediting of Western-centric governance as a whole. Simultaneously, newer mechanisms established by the West, notably the G20, remain under the influence of BRICS nations, with Brazil currently holding the presidency and India scheduled for 2023. The BRICS, led by Russia, are poised to advance with relative freedom, leveraging the political inertia in the West and a limited awareness of the growing appeal of the political value proposition offered by the “other side.” This sets the stage for a compelling agenda aimed at bringing about a paradigm shift[6].

Locked-down Technology and Public Debt don’t mix

When it comes to tech, the trend is towards distrust, as we began to announce back in 2019. The great tech gurus themselves (Elon Musk etc…) are warning of the risks of civilisational drift linked to an AI that has moved into the present in 2023, thanks to ChaptGPT. All notions of free access, open society and worldwide everything are dead and buried. We’re surfing a web where linguistic and national borders have been erected, where international information is barricaded behind paywalls, where countless keywords have been indexed, where the major media and institutions have regained control, where social networks are under intense surveillance…

So much so that good old paper magazines once again look like real windows on the world, despite their obviously narrow angle. The Internet is no longer a citizen, but a merchant. And the most intelligent are now strategising information, understanding and action outside this virtual universe. The icing on the cake, good or bad, is that regulatory bodies with superpowers and methods – notably the UK Competition and Markets Authority (CMA)[7] – are shaking up the world of AI and tech in general. All this will serve a good cause, but also the technological war being waged between the West and the Asians – where the legal weapon of the former will be drawn in an attempt to slow down the pace of innovation of the latter. It remains to be seen how successful this will be.

Against this backdrop, we can confidently anticipate that technology stocks will be hit hard… to the extent that a Nasdaq financial crisis could disrupt the financial world in 2024. But the United States will still be strong enough to absorb a shock which, on the other hand, could have a severe impact on Europe, which is ultra-debt-ridden and in the throes of stasis.

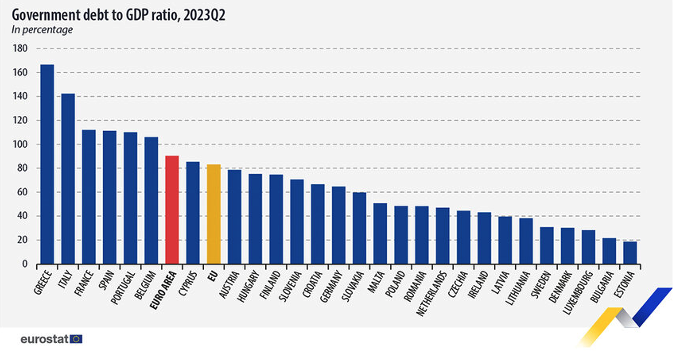

Figure 2 – Public debt of EU Member States in the second quarter of 2023 (% of GDP). Source: Eurostat

In the United Kingdom, nearly one in five councils at risk of bankruptcy. The situation is certainly not very different in many European countries, and just because governments guarantee against the bankruptcy of cities (in France, for example) this does not mean that municipal debt does not represent a major risk of budgetary disruption. High borrowing rates, commercial and business bankruptcies, the impoverishment of the population (and hence the reduction in taxation), government debt levels… combined with the diversion of foreign investment to emerging markets (including the United States), a decline in faith in start-ups and innovation, and the hold of the entire European economy in the Ukrainian crisis, tell us that European finance is preparing to cross some particularly dangerous waters in 2023.

In fact, our team does not believe in the announcements of rate cuts by the European and US central banks, which were probably designed to give the equity markets a bit of breathing space for a short while. In fact, rates will remain high throughout the year: governments need to refinance themselves, to slow the pace of innovation that they are no longer able to keep up with, and to control prices against a backdrop of elections and popular discontent.

While company and business bankruptcies will continue to bite the SME world, reindustrialisation plans will concentrate public funding efforts. The Western world has eaten its fill: the cheap labour of yesteryear is capturing part of the world’s production of consumer goods; to supply everyone, Westerners need to get back to work; immigration has alleviated the problem, but is the subject of much questioning as to the calculation of its cost to public finances; Westerners are therefore going to have to go back to the factory floor. Their fractured social systems, combined with the ever-increasing cost of living, will soon convince them otherwise.

Argentina is showing the way by completing its cuts in social protection to ensure that the population is willing to provide the cheap labour that will enable the country to replace China in the manufacture of products for the American and European markets. But Rishi Sunak in the UK is following the same path, slashing social spending on the pretext of cutting taxes. We see in this policy a real trend that will be implemented in more or less subtle ways in many countries in the Western zone of influence, a trend that we could call “self-colonisation”.

In Europe, a year of social tensions

Europeans will certainly be the most reluctant to bow to these new demands of the geo-economy. And it is a climate of rebellion that we must anticipate on our continent in 2024. In France in particular, the cabinet reshuffles are a clear indication that Macron is anticipating a difficult social year that will require the boat to be firmly lashed down. In Germany, farmers never tire of demonstrating their anger at their government’s support for the free trade advocated by the EU and its allies. But, more generally, the country is a pressure cooker likely to explode in 2024, including in rather hideous forms (violent racist acts, for example). The same goes for Poland, Sweden and elsewhere.

Against this social backdrop, the European elections will provide a faint glimmer of democracy, which will ultimately reflect the despair of citizens by further reinforcing the right-wing bias of the European Parliament. More specifically, we anticipate that the post-election period will begin, as usual, with the distressing spectacle of the inefficiency of the European administrative system in choosing a college of commissioners. This time, however, the likely alliance between the far right and the right of the parliamentary spectrum will save the European institutions, desperate to restore an image of strength to the world, from ridicule. Most probably a very right-wing European Commission will be put in place by the Council of the EU.

The gap is widening

In 2024, a growing divide will be evident between, on one side, the architects of the forthcoming global order—BRICS and the Global South. These entities will sculpt their future trajectories through a political approach emphasizing efficiency over national democratic expression and adopting a multipolar stance in international affairs. On the flip side, the West finds itself ensnared in the present and past, grappling with a near paralysis while awaiting a new beginning from the United States. The Western nations struggle to forge a cohesive momentum, with only a handful of future prospects outlined by a political and economic elite. However, these proposals face rejection from a populace deeply divided within itself.

Should the fear surpass the harm in 2024, it merely signifies a temporary delay. This year will witness the initial tremors, especially in European nations, with consequences echoing into the post-2025 period. Meanwhile, on the global stage, as the divergence between these two regions becomes increasingly evident, it is advisable to steer clear of confrontation. Instead, efforts should focus on fostering fruitful resolutions to peace challenges beyond the year 2024.

_______________

[1] Inversion of the Warren Buffett quote: “Be fearful when others are greedy“, title of an article on China’s Outlook 2024, published by GlobalX, 10/01/2024

[2] A new party, Nouveau Choix, will be competing in the parliamentary elections, with a strategy similar to that of République en Marche, which consists of taking citizens out of the right-left dialectic. If the party wins the 30 seats it is contesting, it could help temper the tough-on-North Korea policy of the country’s current conservative president, Yoon Suk Yeol. Sources: KBSWorld, 18/12/2023; RFI, 11/03/2023

[3] Source: The Korea Herald, 01/01/2024

[4] Source: EastAsiaForum, 04/01/2024

[5] Source: France24, 01/01/2024

Geopolitics: Asymmetrical Recomposition 1 - American election fog disrupts global visibility The fog surrounding the American elections is disrupting global visibility. What will this lack of visibility mean for the [...]

This month we had the pleasure of discussing with Dr. Maria Moloney what 2024 may bring regarding AI and data protection innovation, as well as issues of European and global [...]

Bitcoin: Double-edged institutionalisation The United States' recognition of Bitcoin's legitimacy via the ETFs will be a double-edged sword: it will consolidate the Bitcoin's value and status in the short term; [...]