Since Deng Xiaoping, in the ’70s, gave top priority to economic development[1], China has made tremendous sacrifices. Having worked hard and cheap and polluting its country, it soon became the workshop of the world.

But all those sacrifices were not in vain. Barely 15 years later for instance, in 1993, Shanghai was able to launch its first ultra-modern subway line[2]. This example is not taken at random: the construction of metro lines is always a good indicator of both economic and administrative health of cities or countries.

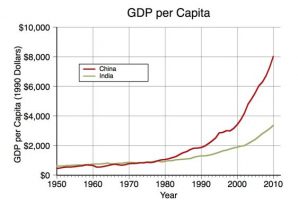

Figure 1 – GDP per capita in China and India, 1950-2010. Source: Wikipedia.

China’s Difficult Global Integration

After the collapse of the Soviet bloc, China accelerated its repositioning in relation to the rest of the world. From the 1990s on, this huge country strengthened the broad and slow process of systemic transition based on a principle of gradual compatibility with the international system.

In economic terms, this is what we call the transition towards the principles of the “western style” market economy, implemented, with the agreement of the Communist Party, by a generation of openly “reformist” economists, among whom the prominent representatives Wu Jinglian[3] or Zhou Xiaochuan[4] (current governor of the People’s Bank of China).

In 1992, the Party decided that resources would be allocated by market forces rather than by state orders; and from 1998 to 2003, an extensive process of deregulation, liberalisation and privatisation was undertaken within the framework of that international compatibility.

The results did not take long to arrive: as of 2001, China was allowed to enter the WTO.

But the arrival of an ultra-dynamic economy of 1.4 billion people into the smooth running international game has provoked a cataclysm which the WTO never fully recovered from[5].

In reality, it is not difficult to understand that as long as globalisation and its institutions were at the service of a single pole of power (the West which had created them in the first place), everything went well. But the arrival of China at the world’s table raised the question of who would actually profit from the game. The Doha Round, initiated one month before China’s integration to the WTO and destined to finalise in three years the liberalisation of world trade (with the avowed objective of developing the third world countries), was blocked by the one who had wished it: the West.

The failure of the Doha Round marks a sustainable reversal of the globalising impulse, simply because, if globalisation at the service of a single pole of power is easy (it is imperialism), the arrival of China in the game has caused a profound structural change in those dynamics by introducing the notion of a multipolar world – in this case “bipolar” but very soon to be followed by India’s perspective as an emerging global mastodon – whilst recent history has been unable to manage multipolarity other than through confrontation.

With one exception: the experiences of regional integration, which have applied principles of flat power structures based on complementarities and win-win logics. It is in these experiences that the world should have looked for the appropriate reorganisation tools of the new global realities. But the model which came out was, ultimately, neither more nor less than a cold war…

Our readers know that we have carefully followed China’s efforts to: integrate smoothly into the existing international system (WTO, G20…); then dilute the China-effect by embarking on the reformist BRICS dynamic, very close to the flat logics of regional integration; attempt to initiate an international monetary reform to lift the US and the world out of the dollar rut[6]; witness the violent attacks of the West against the BRICS attempt[7]; and finally focus on a strategy for the creation of new international institutions initiated by the BRICS or China (OBOR, NDB, AIIB, etc.).

End of the Chinese Patience

Here we are, and so far China has played with patience the card of global integration. In doing so, it has developed a network of commercial, economic, political and strategic partnerships with a growing number of countries and regions, paying particular attention to narrowing the links according to geographical logics. Thus, China initiated a rapprochement based on equality, not with the countries of South-East Asia taken individually, but with their coalition reinforced by a Chinese recognition of their relevance, namely the ASEAN, and despite the presence of notorious “enemies” (Vietnam, Japan, South Korea, the Philippines…).

In a few years, China has won considerable victories, the most recent of which is the ousting of South Korean President Park Geun-Hye, entangled in the threads of the American missile system THAAD, a guarantor of bad long-lasting relations with China; she would probably be replaced by someone more conciliatory with China[8]. The other major progress of Chinese interests in the region is the shift of the Philippines out of US influence.

The US-China crisis in the South China Sea, just like the EU-Russia crisis in Ukraine, should have been an opportunity to create new lines of cooperation among these regions, and between China and the United States. Instead, conflicts have become harder and the logics of “you’re either with me or against me” have imposed themselves, forcing countries to take a stand; whereas the only way to guarantee their relative independence would be precisely not to impose anyone to make such choices.

Since 2014 and the Ukrainian crisis, the world is thus gradually structured into two opposing camps; with the multipolar BRICS also having to comply with this rule. And the US-China one-to-one is fast approaching.

This is how the United States will try to associate Russia to its camp in the coming months. Whilst China, via the New Silk Road, will try one last time to associate Europe to its own.

Our team is still looking at the last rays of hope likely to move us away from this dark scenario, such as the arrival of Antonio Guterres[9], the Portuguese reformist, at the head of the UN, or the strengthening of the G20 as a global political platform under the impulse of China and, hopefully, relayed by Germany in July 2017[10]; or the prospects to reorganise the Middle East in the wake of the end of the Syrian war. But it is still difficult to stay optimistic when we look lucidly where the heavy tendencies send us.

The current state of the Chinese positioning in the world makes it possible to see the following:

. the deployment of its zone of influence henceforth comes up against some pitfalls which point out its unexceedable limits: India on one side (with its large demonetisation plan, India has got rid of its financial dependence on China, which does not necessarily bode well for the future of relations between the two giants), Japan on the other (a country which is not yet ready to free itself from the US strategic tutelage);

. on the other hand, as we have just seen, the conditions are somehow met for good cooperation with ASEAN, knowing the gigantic infrastructure projects correspond to real financing needs of the region and, as such, are irresistible;

. the financial system based on the Yuan, considerably reinforced by China’s massive sales of foreign reserves and their change into Yuan, is now a reality, ready to integrate a multi-currency international financial system, but also, if rejected, ready to focus on regional logics.

China is clearly at the end of a long series of attempts to become globally compatible: positive participation in international forums, vast internal economic reforms, transnational investment projects and the creation of ad hoc tools. China is now ready; in a similar way to Russia which, in 2013, was ready to make its official entry on the international scene and relied on its Olympic Games to mark this recognition. But…

China versus the United States

But America closes itself and gets positioned on a clearly conflictual axis face to China.

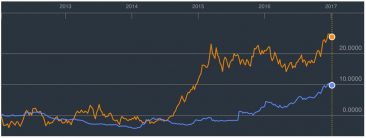

In particular, there is the threat of accusing China of manipulating its currency[11], which would make possible “legal” sanctions of a protectionist nature (yet, since when does the United States need a legal framework to do so?). However, when we look at the following chart, which compares the evolution of the dollar index (value of the dollar against a basket of currencies composed of euro, yen, sterling pound, Canadian dollar, Swedish crown and Swiss franc) and that of the dollar against the Yuan, we see the bad faith of the US: since 2014, the Yuan has fallen against the dollar half as much as the mentioned basket of Western currencies…

Figure 2 – In orange: evolution of the dollar index; in blue: evolution of the dollar against the Yuan, 2012-2017. Evolution percentage, against the reference point of January 2012. Source: Bloomberg.

The same threat would therefore be much more “justified” towards the euro zone, Japan or the United Kingdom, and yet China is the target. It is obviously a political motivation that drives the United States, much more than economic reality. This is the same logic as the appointment of ministers notoriously hostile to China[12] at the head of the next government (which could by the way be seen as incoherent with the new friendship displayed towards Russia, but that is not the only incoherence of the President-elect).

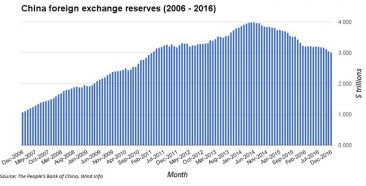

These accusations are all the more difficult for China to accept that in reality it actively limits the depreciation of its currency. Indeed, it sells its enormous foreign exchange reserves at the rate of about $40 billion a month to buy the Yuan and consequently support its own currency.

Figure 3 – Chinese foreign reserves in trillions of dollars, 2006-2016. Source: CNBC.

Since August 2014, Chinese reserves have fallen by almost 25% when measured in dollars. It should be noted, however, that those figures (which are evidenced in the economic media) has no interest from the Chinese point of view, since only the value of their reserves in Yuan is truly important. And since it took 6.15 Yuans for one dollar in August 2014, and now it takes 6.95, it has dropped “only” by 15%, a little more reasonable…

It is not for the labour’s sake that China supports its currency, since it is still largely focused on exportations, and therefore a weak Yuan is needed[13]. In this respect, investors expect a growing decline of the Yuan, which explains the capital outflow the country suffers from (exchange of Yuan in dollars especially to save the value of investments in case of a Yuan decline). According to some estimates[14] (from Anglo-Saxon financial reports, as usual, unfortunately), between 600 and 800 billion dollars have been taken out of the country in 2016, and even more so in 2015. Yes, that is really a lot.

Login

Crypto-currencies, of which Bitcoin is the most popular, are "virtual" currencies devoid of any physical reality, possessing an electronic form and functioning by using cryptographic methods. They are used specially [...]

Every year, LEAP/E2020 is offering you a short overview of the up and down trends of the year which is starting. In addition to the intellectual interest of this contribution [...]

Currencies: Watch out, Turbulence Ahead The currency market is particularly dangerous this year: with a dollar which has strengthened whilst Trump needs a weak currency and will do everything possible [...]