GEAB 108

The United States has been voluntarily isolating itself from the rest of the world, and not just from a geopolitical point of view. This terrible isolation can only get worse, whatever the result of the presidential election: if Trump wins, it will be due to a lack of foreign policy; in the case of Clinton, her iron-fist will have a word. Another domain, namely finance, which has so far been spared, is being added to this political dimension; something which has always been at the centre of America’s power in the world. No wonder this happens at the very moment the US can no longer hold itself.

The Deutsche Bank case: a very useful scarecrow

When in trouble, the US always uses the same method, which consists of hiding its own problems by bringing out into the open the problems of others. Europe is regularly the fall guy. So when the world, in total awe, learns about the record fine of $14 billion that the United States imposed on Deutsche Bank[1], one could certainly look horrified at the violations committed by this bank[2], but one must also see the interest which this sanction serves. Many commentators saw this as a little revenge after the Apple fine in Europe[3], a credible explanation, but there is more to this. By creating problems for the largest European bank, the United States has managed to bring about debates on the problems of European banks in general. Despite the surprising financial stability in Europe after all those years of turmoil (in part thanks to the ECB’s capital injections, even though they probably serve global finance more than European interests), we do not claim that the European banking industry is in perfect shape, far from it[4]. But we think this is a quite convenient bogeyman to forget about the current US difficulties. The titles of articles about Deutsche Bank are definitely alarmist: imminent bankruptcy, bailout necessary, a contagion to other European banks, or even a possible next crisis in sight[5].

And indeed, not to mention the so called economic growth of the United States, which is worse and worse as seen on the following chart[6], the Fed’s failure to raise interest rates is indicative of the weakness of the US economy.

Figure 1 – Quaterly Official Growth of the US economy (annualised rhythm) since January 2015.

Source: Trading Economics.

The job market is still struggling, despite the announcement of an unemployment level of around only 5%, which does not reflect reality at all when we look at the lowest employment rate since 1970 (to sum up, the decline in the unemployment rate is only the fruit of the decline in the participation rate).

Figure 2 – Labour participation rate (blue, left scale) and unemployment rate (red, right scale) in the US since 2007. Source: FRED.

Another example: despite an always higher dollar, Bayer affords to buy back Monsanto[7] and Danone bought back WhiteWave[8]: as if Old Europe could have afforded the luxury to buy the US (contrary to what we saw last year). We could give more examples like these, but we got it: the real economy is not doing better in the US (how could it? by hardly caricaturing, we could say that only the finance was helped and still nothing has changed since 2008…). Amid the ambient complacency for the United States, it still says here and there[9] that American banks are not in better shape than before 2008, despite the “reforms” and legal obligations. Yet, the world speaks only of Deutsche Bank (DB) and the weakness of other European banks. It says that there is little or no risk of contagion to US banks, even though such risk is real since Deutsche Bank is considered one of the banks with the largest systemic risk. We must therefore believe that something big is being hidden there…

Of course, doubts (which are justified) about the strength of European banks have never really disappeared. But the trigger for the current turmoil is definitely this US fine which Deutsche Bank is not ready and able to pay[10]. Isn’t it amazing that the US imposed such a high fine, which apparently Deutsche Bank is unabe to pay, and thus runs the risk of breaking the whole banking system into pieces?

The case of Deutsche Bank is obviously a bluff. We are talking of a systemic bank, the collapse of which would hurt everyone, including and especially the US banks. Since the goal is certainly not to break the DB, it is important to look for the real reasons of the attack; diverting the media’s attention away from US failures and possibly also an attempt to put pressure on Merkel. This is why we wanted to do the exact opposite of what we were invited by the media to do, by looking towards the spot the attack came from…

Wall Street to be abandoned by the Financial Sector?

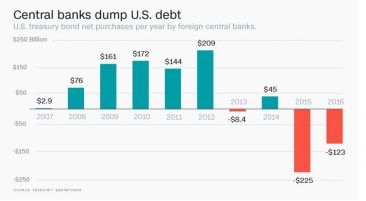

But some camouflage was indeed needed to cover up the bad news that accumulates in the finance sector. And the bad news comes from the largest buyers of US Treasury bonds: the foreign central banks from China and Russia, but also from Japan, Saudi Arabia and Europe. They are all selling massively, at a historic pace, US Treasury bonds which they had patiently accumulated over time[11]. Oh sure, each of them supposedly has good domestic reasons to do so: basically, Anglo-Saxon media state that the aim is to have their currency go up, after the decline in their weakened economy.

For Russia this is probably partially true as the rouble was down for a while, bringing a worrying level of inflation. But clearly the central bank prefers to buy gold instead of roubles, which somewhat contradicts the aforementioned Anglo-Saxon official media version.

China would sell for similar reasons, since nothing goes well for them anymore; its growth rate fell below the 7% mark and the yuan lost 10% from its highest level two and a half years ago (what a horror). Again, we need some explanations as to why China buys gold instead of US Treasury bonds, and why China prefers to first get rid of its shares from the US financial markets[12]: does China anticipate a stock market crash in the United States?

The explanation given by Saudi Arabia is, obviously that oil is too cheap and, for European countries and Japan, because of the economic decline.

So all is well and there is no visible link with the health of the United States, of course. It is only a coincidence that all these countries are selling massively their US obligations.

Figure 3 – US treasury bonds’ net annual purchases by foreign central banks, 2007-2016. Source: CNN.

Some people dare to say that this is a request that the Fed would send to other central banks, aiming to bring the dollar down. But the dollar did not fall and the risk with such a request is so real and so dangerous that Yellen would never take it. To bury this hypothesis once and for all, we note that China is not only selling its treasury bonds, as already mentioned, but also, and especially, its stock of US shares, risking potential chaos on the US markets. Moreover, it is probably a sign of even greater distrust, something that the Fed would never ask for. So definitely no, the illusion that the Fed and the US are behind these movements does not hold up.

Part of the US strategy is based on the fact that US Treasury bonds are supposed to represent a “safe haven” in this storm: and indeed, as usual, the panic created around the European banks (a wind blown by the Anglo-Saxon media) allowed to temporarily bring the pack of investors towards US bonds. Good timing, because the sale of these bonds started to become difficult: some of the media have even been worried about weak investor demands[13], especially for long maturity bonds (30 year-long ones). However, this feeling of treasuries “safe haven” starts to dissipate, because the hedge funds and money market funds would also sell their US bonds[14] … For now, despite the low demand, the interest rate increase remains moderate and it is far from the level we saw at the end of 2013 to the beginning of 2014, but for how long? If the increase becomes crazy, the Fed will be forced to again adopt some new “unconventional” measures; but will it still be credible this way?

Login

Political anticipation does not work using crystal balls. "Future data" represents the raw material for its analyses: elections, summits, and various meetings are elements which allow us to cast light [...]

When members of the UN Security Council wage war at each other... It is clear that in a supposedly common struggle against a common enemy - the Islamic State - [...]

In short, the answer is, not much. But let’s elaborate! As our team noted in the September issue, Brexit unleashed a large potential to reorganise Europe with, as it happens [...]

Both in the United States and around the world, this news has been making some noise: since October the 1st, the internet is finally "free from US tutelage." Is it, [...]

It is time to get rid of Western Sovereign Bonds Following the previous article on the topic of US Treasuries, it seems clear to our team that it is best [...]